This means that this decade, you must cut in half your own emissions. That’s both Scope 1 and Scope 2 emissions, as well as those Scope 3 emissions related to employee commuting, business travel including accommodation, employees working from home, water usage, waste and purchased goods and services.

Where other Scope 3 emissions are material to your total emissions and where data allows you to measure it, your company should also aim to cut Scope 3 emissions in half this decade.

But how do you know what Scope 3 emissions are material (or most relevant) to your business?

Materiality assessment

To asses their material issues, many large businesses carry out materiality assessments, which involve interviewing stakeholders to understand their concerns and researching global issues and trends. This insight is plotted onto a matrix to pull out the most relevant issues to the business.

We understand that this could be too complicated or time consuming for SMEs, so if you want to understand what other Scope 3 emissions you should be looking to measure and reduce, you can use our Scope 3 materiality checklist as a starting point.

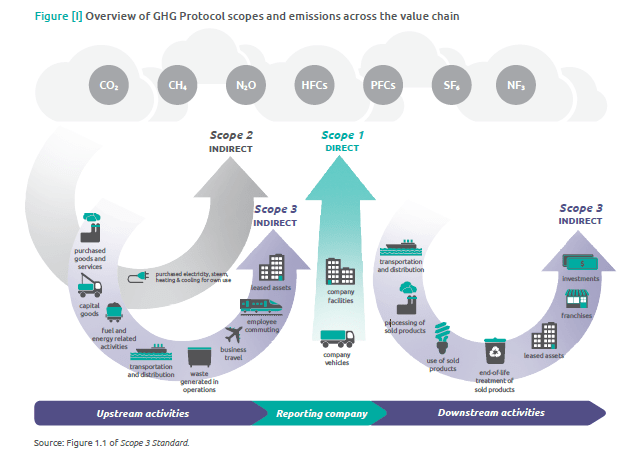

What are Scope 3 emissions?

To understand your Scope 3 emissions, you first need to be clear on what’s included in Scopes 1 and 2.

Scope 1 covers your direct emissions from owned or controlled sources (gas and company vehicles). Scope 2 covers your indirect emissions from the generation of purchased electricity, steam, heating and cooling consumed by your business.

Scope 3 includes all other indirect emissions that occur in your value chain, as shown in the diagram and list from the Greenhouse Gas Protocol below.